The good news is…you have made it to 65 years young. Happy Birthday!

The bad news is…you will start receiving mail regarding Medicare approximately 8 months before you get to blow out the candles. Some of the mail is from the Social Security Administration; however, most of it is from insurance companies and insurance agents.

The ugly part is the learning curve.

Hopefully, after reading this article, you will cherish this little birthday gift.

Where to start?

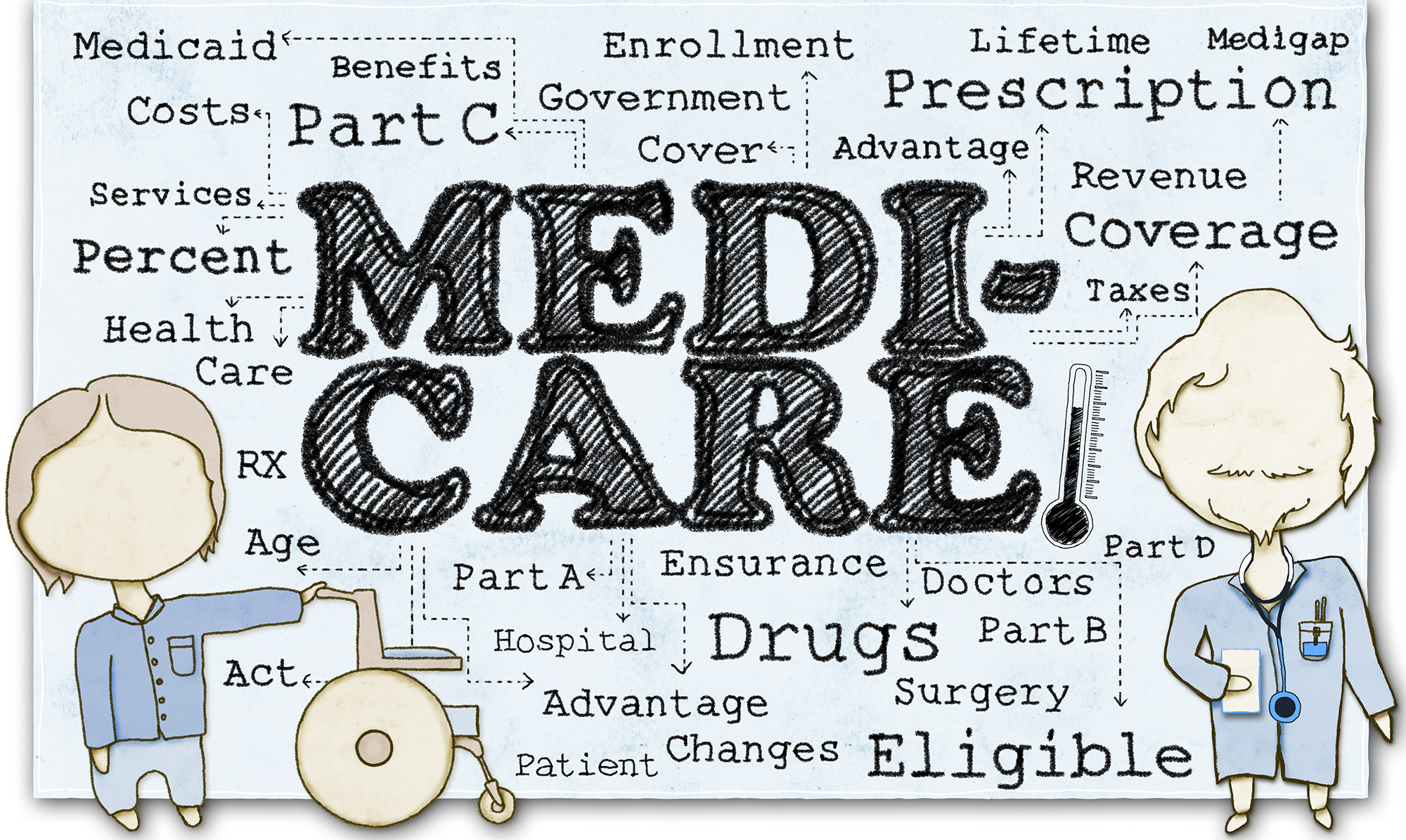

Here are the many “parts” to Medicare which can be confusing:

Part A covers hospitalization (most people have worked to have hospitalization provided).

Part B covers doctors and outpatient visits (the government charges a premium for this).

Part A + Part B is “original Medicare” which pays approximately 80% of your medical expenditures.

Part C is the Medicare Advantage Plan which provides Parts A and B, plus extra benefits and Part D.

Part D is prescription drug coverage.

Supplements

Then, there are “supplements.” These insurance “plans” (not “parts”) are purchased by the consumer from insurance companies with the assistance of an agent. These plans (A, B, C, D, F, G, K, L, M, or N) help fill in some – or most – of the coverage that original Medicare does not cover. The most comprehensive Plan is F.

Supplemental plans allow you to obtain medical care anywhere, provided the doctor accepts original Medicare.

Part C is known as a Medicare Advantage Plan. These plans are HMO plans. They are affiliated with a network of primary doctors. Someone on this type of plan would select a primary care physician (PCP) from a contracted network. Referrals to a specialty doctor would be necessary. Medical care must be sought within a geographic area, unless it is an emergency or on an urgent care basis.

Most of these plans in our area are offered at zero premiums and include Part D. They also provide some additional benefits that are not available with original Medicare such as a basic fitness membership, transportation, vision and a nurse hotline, to name a few.

Part D stands for “drugs.” If you choose to enroll in a Part D plan, you can only do so through a private insurance company that is contracted with Medicare. While the government does not require you to have a Part D, should you wish to join a plan later, it will impose a late enrollment penalty or LED. The lifetime penalty will be in addition to your premium payment.

This information is a general overview and there are additional rules, regulations, premiums, enrollment periods, medical care and coverage items you should consider before jumping into the Medicare world.

Starting in 2020, there are new regulations regarding Supplement Plans F and C and their future availability; the Medicare Access and CHIP Reauthorization Act of 2015 (MACRA) will be making an impact.

Therefore, read, research and/or partner with a licensed professional to help make the transition into Medicare a happy one.

Cindy Kleine is an independent sales agent with Kleine Financial & Insurance Solutions, Inc. in Palm Desert. Serving the Coachella Valley (license #0B7732). For more information, call (760) 346.9700.

Comments (0)